Mike Zigmont, author of the Zigmont Report, is a partner at New York-based Harvest Volatility Management, a hedge fund with over $12B AUM, offering volatility management solutions to its investor base worldwide. Mike has been publishing his daily newsletter (Monday-Friday) privately for the firm’s investors and his personal contacts in the investment business

Mike Zigmont, author of the Zigmont Report, is a partner at New York-based Harvest Volatility Management, a hedge fund with over $12B AUM, offering volatility management solutions to its investor base worldwide. Mike has been publishing his daily newsletter (Monday-Friday) privately for the firm’s investors and his personal contacts in the investment business

since 2008, sending it daily shortly after the market close.

The opinions expressed below are my own

Hope springs eternal. Overseas markets rallied last night and this morning and our premarket got hot-to-trot. Enthusiasm didn’t wane with regular trading and the tape meandered higher through the session. Capital flow was light again at 94%. The news today was thin again. The tariff-inspired drop from yesterday was unwound, and then some.

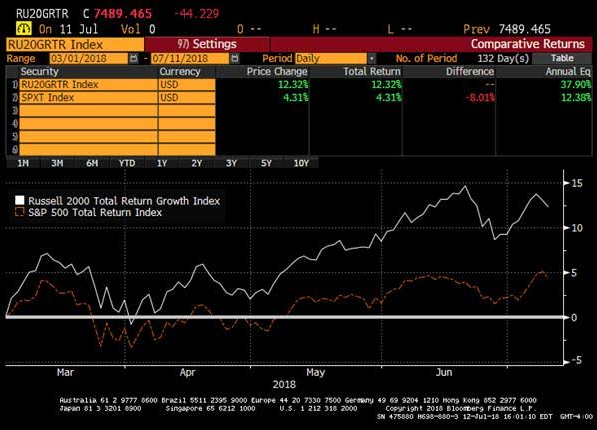

The NASDAQ-100 led things today and it set new all-time highs. The bullishness for tech, and growth more generally, is borderline mania. The relative performance of growth vs the market has trended extremely strongly since the beginning of March.

Here’s the performance difference since then.

This divergence feels very much like investors are chasing returns and we’re inside a positive feedback loop. You can’t swing a dead cat without hitting someone on CNBC trumpeting the performance of Netflix or Amazon or Nvidia (if you want some anecdotal examples).

Those stocks are beyond hot. They are up 118%, 50%, and 28% respectively.

I can only imagine how many investors are piling into these names. Fear of missing out (FOMO) feels like it is not in effect for the whole market (like in 2016 and 2017). FOMO feels like it’s migrated. It’s moved into the best performing names.

Only when one of those hot stocks stumble fundamentally, will the process unwind. It will be ugly. I doubt it beginstomorrow

. JP Morgan announcestomorrow

. It’s a stone cold lead pipe lock that they beat analyst expectations.It’s a 50/50 proposition that the broader market extrapolates for itself, from JPM’s results.

See you then,

Mike